![]()

![]()

![]()

![]()

The official (CRAN) version of the package can be installed using

install.packages("corbouli")Alternatively, the development version of the package can be installed via

if (!require(remotes)) install.packages("remotes")

remotes::install_github("cadam00/corbouli")To cite the official (CRAN) version of the package, please use

Adam, C. (2025). corbouli: Corbae-Ouliaris Frequency Domain Filtering. R package version 0.1.5. doi:10.32614/CRAN.package.corbouli

Alternatively, to cite the latest development version, please use:

Adam, C. (2025). corbouli: Corbae-Ouliaris Frequency Domain Filtering. (v0.1.5). Zenodo. doi:10.5281/zenodo.13740089

Corbae and Ouliaris (2006) Frequency Domain Filter is used for extracting cycles from either both on stationary and non-stationary time series. This is one approximation of the ideal band pass filter of the series. The result is close to the one of the Baxter-King (1999) filter, but end-points are directly estimated and so facing the end-point issue is not faced.

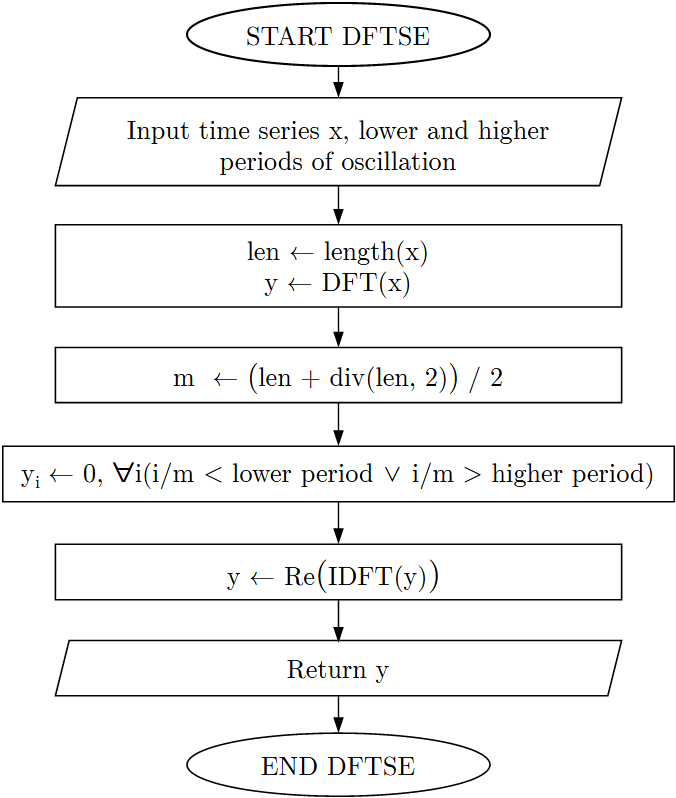

The main idea of this filtering algorithm is illustrated in Fig. 1 and 2. The main

idea of the DFTSE subroutine is shown in Fig. 1, where DFT (Discrete Fourier Transform) of the

times series, then frequencies lower and higher by periods of

oscillation thresholds are assigned to zero and finally IDFT (Inverse

Discrete Fourier Transform) are performed. Additional implementation

details of this subroutine can be found at source code of the function

corbouli::dftse.

Fig. 1: DFTSE subroutine.

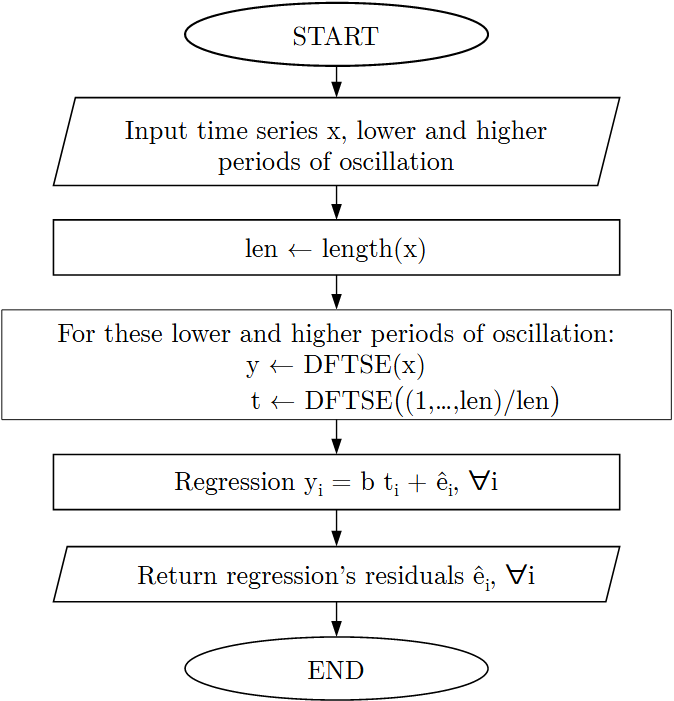

The final algorithm is described in Fig. 2, where filtered series is the residuals of the regression of \(DFTSE(x)\) on \(DFTSE\) of the normalized trend.

Fig. 2: Corbae-Ouliaris main algorithm.

The minimum and the maximum periods of oscillation should be determined when using this method, so as to irrelevant to filtering frequencies are removed. As an example from Shaw (1947), a business cycle usually has a lower period of 1.5 years and a higher period of 8 years. This information can be used while for filtering as expressed from the following Table 1.

| Sample Frequency | Lower | Higher |

| Month | 18 | 96 |

| Quarter | 6 | 32 |

| Year | 2 | 8 |

Table 1: Lower and higher periods of oscillation.

The same table in fragments of \(\pi\) can be transformed into the Table 2 using the \(lower\ frequency = 2 / higher\ period\) and \(higher\ frequency = 2 / lower\ period\). For instance, for quarterly sampled time series, we have \(lower\ frequency = 2 / 32 = 0.0625\) and \(higher\ frequency = 2 / 6 = 0.3333\).

| Sample Frequency | Lower | Higher |

| Month | 0.0208 | 0.1111 |

| Quarter | 0.0625 | 0.3333 |

| Year | 0.25 | 1 |

Table 2: Low and high frequency in fragments of \(\pi\).

The longer the series, the more the long run frequency is expressed by a lower frequency as fragment of \(\pi\) equal to 0. Moreover, the output gap can be expressed using higher frequency as fragment of \(\pi\) equal to 1 (Ouliaris, 2009).

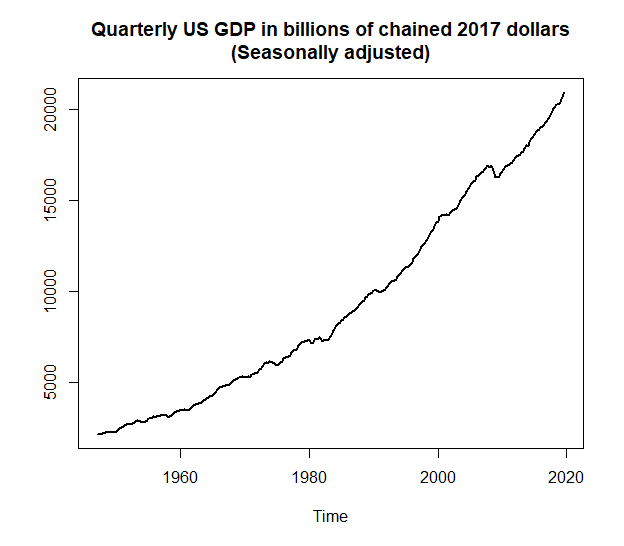

For this example, the quarterly US GDP in billions of chained 2017 dollars (Seasonally adjusted) will be used.

# Import package to workspace

library(corbouli)

# Import "USgdp" dataset

data(USgdp)

plot(USgdp, main = "Quarterly US GDP in billions of chained 2017 dollars

(Seasonally adjusted)", ylab = "", lwd = 2)

Fig. 3: USgdp dataset.

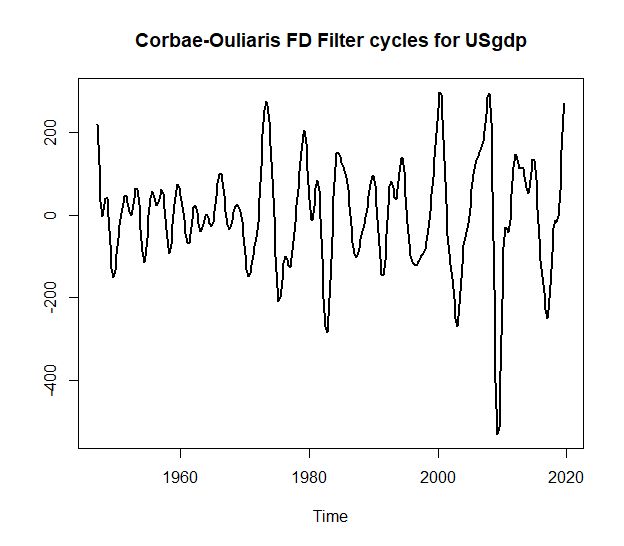

# Extract cycles

co <- corbae_ouliaris(USgdp, low_freq = 0.0625, high_freq = 0.3333)

# Plot cycles of filtered series

plot(co,

main = "Corbae-Ouliaris FD Filter cycles for USgdp",

ylab = "",

lwd = 2)

Fig. 4: Corbae-Ouliaris FD Filter cycles.

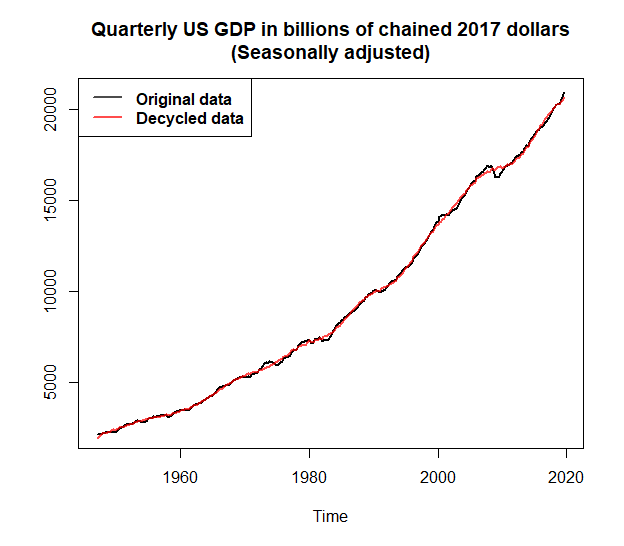

# Plot real data with the ones after removing cycles

# Removing cycles from original data

USgdp_rmco <- USgdp - co

# Plot Original vs Decycled data

plot(USgdp, main = "Quarterly US GDP in billions of chained 2017 dollars

(Seasonally adjusted)", col = "black", lwd = 2, ylab = "")

lines(USgdp_rmco, col = adjustcolor("red", alpha.f = 0.7), lwd = 2)

legend(x = "topleft", lwd = 2, text.font = 2,

col= adjustcolor(c("black","red"), alpha.f = 0.7),

legend=c("Original data", "Decycled data"))

Fig. 5: Original vs Decycled USgdp data.

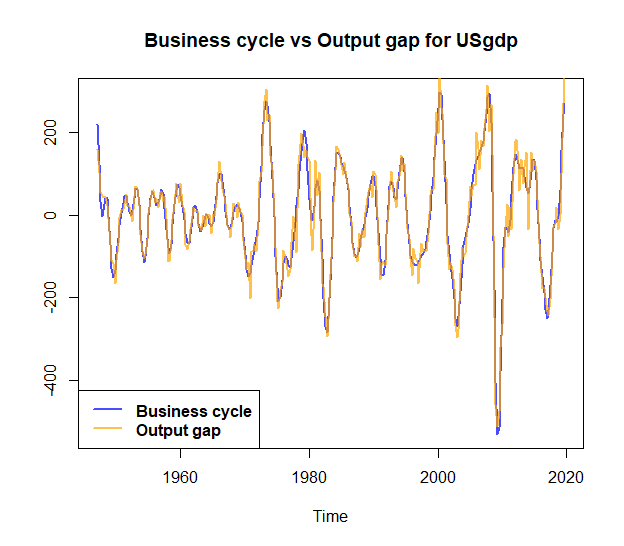

As noted by Ouliaris (2009), for

setting high_freq = 1 the output gap series than business

cycle one will have higher volatility (Fig. 6).

# Extract output gap

og <- corbae_ouliaris(USgdp, low_freq = 0.0625, high_freq = 1)

# Plot Business cycle vs Output gap

plot(co, main = "Business cycle vs Output gap for USgdp",

col = adjustcolor("blue", alpha.f = 0.7), lwd = 2, ylab = "")

lines(og, col = adjustcolor("orange", alpha.f = 0.7), lwd = 2)

legend(x = "bottomleft", lwd = 2, text.font = 2,

col= adjustcolor(c("blue","orange"), alpha.f = 0.7),

legend=c("Business cycle", "Output gap"))

Fig. 6: Business cycle vs Output gap.

Baxter, M., & King, R. (1999), Measuring Business Cycles: Approximate Band-Pass Filters for Economic Time Series. Review of Economics and Statistics 81(4), pp. 575-593.

Corbae, D., Ouliaris, S., & Phillips, P. (2002), Band Spectral Regression with Trending-Data. Econometrica 70(3), pp. 1067-1109.

Corbae, D. & Ouliaris, S. (2006), Extracting Cycles from Nonstationary Data,in Corbae D., Durlauf S.N., & Hansen B.E. (eds.). Econometric Theory and Practice: Frontiers of Analysis and Applied Research. Cambridge: Cambridge University Press, pp. 167–177. doi:10.1017/CBO9781139164863.008

Ouliaris, S. (2009), Ideal Band Pass Filter For Stationary/Non-Stationary Series.

Pérez Pérez, J. (2011), COULIARI: Stata module to implement Corbae-Ouliaris frequency domain filter to time series data. Statistical Software Components, S457218, Boston College Department of Economics.

Shaw, E.S. (1947), Burns and Mitchell on Business Cycles. Journal of Political Economy, 55(4): pp. 281-298. doi:10.1086/256533