bayesestdft:

Estimating the degrees of freedom of the Student’s t-distribution

under a Bayesian frameworkSomjit Roy, Department of Statistics, Texas A&M University. Email: sroy_123@tamu.edu

Se Yoon Lee, Department of Statistics, Texas A&M University. Email: seyonlee.stat.math@gmail.com

bayesestdft is an R package providing tools to implement

Bayesian estimation of the degrees of

freedom in the Student’s t-distribution, that

are developed in Lee

(2022). Estimation experiments are run both on simulated as well as

real data, where broadly three Markov Chain Monte Carlo

(MCMC) sampling algorithms are used: (i) random

walk Metropolis (RMW), (ii)

Metropolis-adjusted Langevin Algorithm (MALA)

and (iii) Elliptical Slice Sampler (ESS)

respectively, to sample from the posterior distribution of the degrees

of freedom.

The current version of the package bayesestdft 1.0.0

provides Bayesian routines to estimate the degrees of freedom of the

Student’s t-distribution with Jeffreys prior

(BayesJeffreys), Gamma prior

(BayesGA), and Log-normal prior

(BayesLNP) endowed upon as the prior distribution over the

degrees of freedom. MALA is used to draw posterior

samples in case of the Jeffreys prior, hence to operate the function

BayesJeffreys, the user needs to install the

numDeriv R package. For more technical insights into

bayesestdft, refer to the slides.

bayesestdftbayesestdft.numDeriv and

dplyr.Now bayesestdft can be installed from both

Github and CRAN respectively, using

the following lines of code:

library(devtools)

devtools::install_github("Roy-SR-007/bayesestdft")

library(bayesestdft)install.packages("bayesestdft")

library(bayesestdft)bayesestdft facilitates a full Bayesian

framework for the estimation of the

degrees of freedom in the Student’s

t-distribution. More precisely, given \(N\) independent and identical samples \(x = (x_1,x_2, \cdots, x_N)\) from the

Student’s t-distribution:

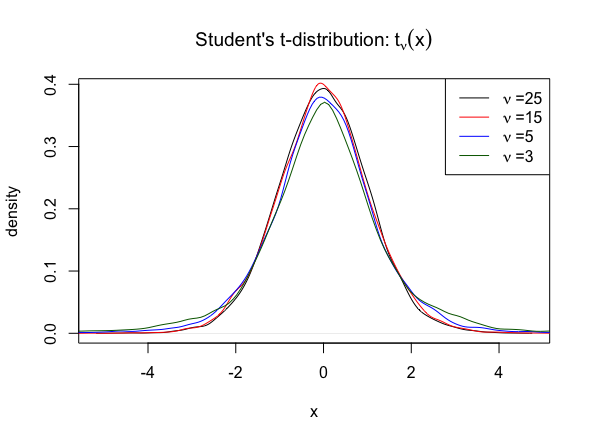

\[ t_{\nu}(x) = \frac{\Gamma\left( \frac{\nu+1}{2} \right)}{\sqrt{\nu \pi} \Gamma\left( \frac{\nu}{2} \right)} \left(1 + \frac{x^2}{\nu} \right)^{-\frac{\nu +1}{2}}, \quad x \in \mathbb{R} \]

and a prior distribution \(\pi(\nu)\) over the degrees of freedom \(\nu\), the aim is to sample from the posterior distribution:

\[ \pi(\nu|\textbf{x}) = \frac{\left[\prod_{i=1}^{N} t_{\nu}(x_i) \right]\cdot \pi(\nu)}{\int_{\mathbb{R}^{+}} \left[\prod_{i=1}^{N} t_{\nu}(x_i)\right] \cdot \pi(\nu) d\nu}, \quad \nu \in \mathbb{R}^+ \]

The current version of the package bayesestdft 1.0.0,

provides four prior choices \(\pi(\nu)\) viz., the

Jeffreys prior \(\pi_J(\nu)\), an

exponential prior \(\pi_E(\nu)\), a gamma

prior \(\pi_G(\nu)\), and a

log-normal prior \(\pi_L(\nu)\).

\[ \pi_{J}(\nu) \propto \left(\frac{\nu}{\nu+3} \right)^{1/2} \left( \psi'\left(\frac{\nu}{2}\right) -\psi'\left(\frac{\nu+1}{2}\right) -\frac{2(\nu + 3)}{\nu(\nu+1)^2}\right)^{1/2},\quad \nu \in \mathbb{R}^+\]

where \(\psi(a) =

\frac{d\log\Gamma(a)}{da}\) and \(\psi'(a) = \frac{d\Psi(a)}{da}\) are

the digamma and trigamma functions

respectively, which are computed using the R functions

digamma() and trigamma() in the

base package.

BayesJeffreysWe consider \(N=100\) simulated

observations \(x = (x_1, x_2, \cdot,

x_N)\) from \(t_{0.1}\)

distribution, where the degrees of freedom is \(\nu = 0.1\). We estimate \(\nu\) using the Jeffreys

prior and consider posterior samples from both RMW and

MALA MCMC sampling engines. The corresponding R code

for using the function BayesJeffreys() to sample from the

posterior with a Jeffreys prior over the degrees of

freedom \(\nu\) is:

x = rt(n = 100, df = 0.1)

# simulating S = 10000 posterior samples

nu1 = BayesJeffreys(x, S = 10000, sampling.alg = "MH")

nu2 = BayesJeffreys(x, S = 10000, sampling.alg = "MALA")

# posterior mean estimate from the RMW algorithm

mean(nu1)

# posterior mean estimate from the MALA sampling scheme

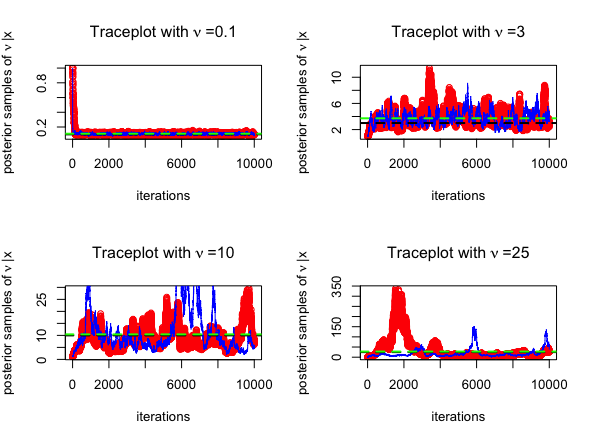

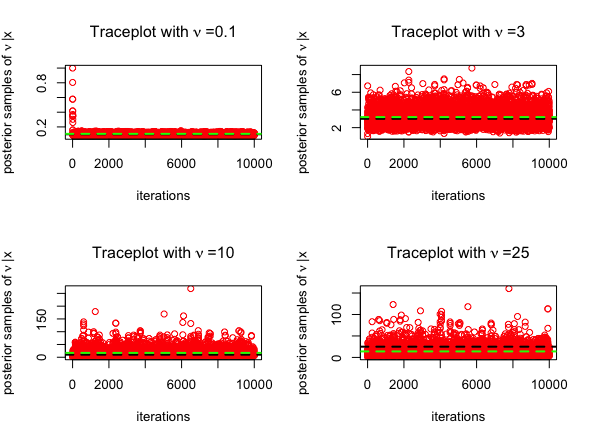

mean(nu2)The trace plots for MCMC algorithms (posterior samples obtained from RWM in red and those obtained from MALA in blue) are given below, for \(\nu = 0.1, 3, 10, 25\). The posterior mean is highlighted in green below.

\[ \pi_{E}(\nu) =Ga(\nu|1,0.1) = Exp(\nu|0.1) = \frac{1}{10} e^{-\nu/10},\quad \nu \in \mathbb{R}^+\]

where the rate hyper-parameter has been set to \(0.1\) following Fernández and Steel (1998).

BayesGAOnce again, we consider \(N=100\)

simulated observations \(x = (x_1, x_2, \cdot,

x_N)\) from \(t_{0.1}\)

distribution, where the degrees of freedom is \(\nu = 0.1\). We estimate \(\nu\) using the

Exponential prior and consider posterior samples from

RMW MCMC scheme. Following is the R code for using the

function BayesGA():

x = rt(n = 100, df = 0.1)

# simulating S = 10000 posterior samples

nu = BayesGA(x, S = 10000, a = 1, b = 0.1)

# posterior mean estimate

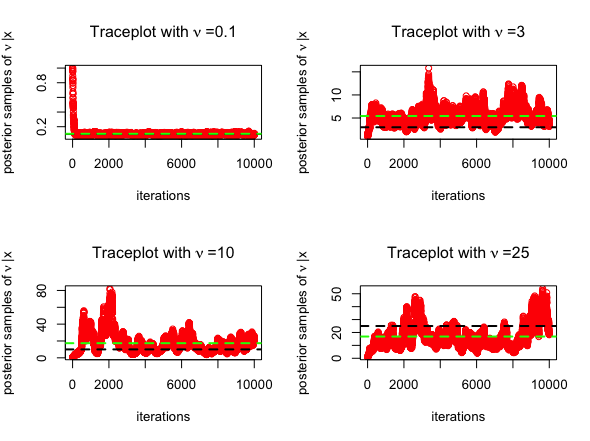

mean(nu)The trace plots for MCMC algorithm (posterior samples obtained from RWM in red) are given below, for \(\nu = 0.1, 3, 10, 25\). The posterior mean is highlighted in green below.

\[ \pi_{G}(\nu) =Ga(\nu|2,0.1) =\frac{\nu}{100} e^{-\nu/10},\quad \nu \in \mathbb{R}^+\]

where the shape and rate hyper-parameters are set to \(2\) and \(0.1\) respectively, as recommended by Juárez and Steel (2010).

BayesGAThe BayesGA() function is implemented with the same

configuration as above in case of the Exponential prior

with a slight generalization of inducing a Gamma prior

over \(\nu\). To what follows, is the R

code for using BayesGA() under the Gamma prior set up with

posterior sampling being done using the RWM scheme:

x = rt(n = 100, df = 0.1)

# simulating S = 10000 posterior samples

nu = BayesGA(x, S = 10000, a = 2, b = 0.1)

# posterior mean estimate

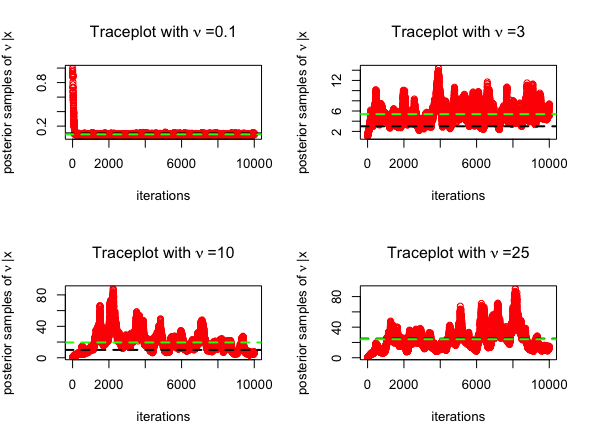

mean(nu)The trace plots for MCMC algorithm (posterior samples obtained from RWM in red) are given below, for \(\nu = 0.1, 3, 10, 25\). The posterior mean is highlighted in green below.

The Log-normal prior has been suggested as a viable option in Lee (2022) with the choice of mean and variance hyper-parameters as \(1\), a justification to which has been provided through the sensitivity analysis done in Section 4.1 of Lee (2022).

\[ \pi_{L}(\nu) =logN(\nu|1,1) =\frac{1}{\nu \sqrt{2\pi}} \exp\left[- \frac{(\log \nu - 1)^2}{2} \right],\quad \nu \in \mathbb{R}^+\]

BayesLNPThe BayesLNP() function draws posterior samples using

the Elliptical Slice Sampler (ESS),

considering a Log-normal prior over the degrees of

freedom \(\nu\), and the R code for its

implementation is given below:

x = rt(n = 100, df = 0.1)

# simulating S = 10000 posterior samples

nu = BayesLNP(x, S = 10000)

# posterior mean estimate

mean(nu)The trace plots for MCMC algorithm (posterior samples obtained from ESS in red) are given below, for \(\nu = 0.1, 3, 10, 25\). The posterior mean is highlighted in green below.

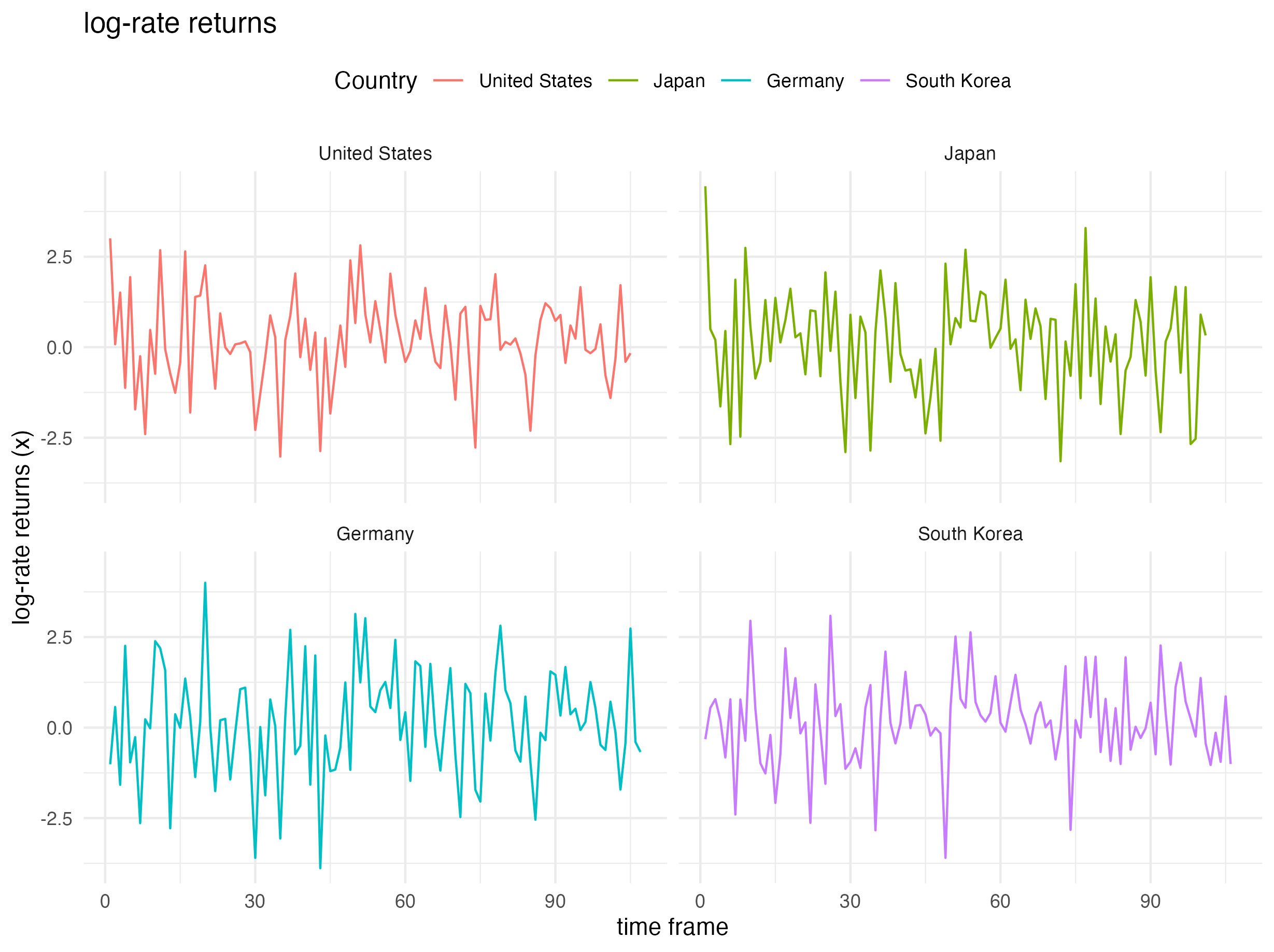

Heavy-tailed daily stock return index values were considered for four countries: (i) United States (S&P500), (ii) Japan (NIKKEI225), (iii) Germany (DAX Index), and (iv) South Korea (KOSPI). Particularly, the data of United States (S&P500) from June 02, 2009 through October 30, 2009 is picked up for analysis resulting into a sample size of \(N = 100\) observations.

The log-rate returns (multiplied by \(100\)): \(x_i = \log\left(X_{i+1}/X_{i}\right)\times 100\) is modeled, where \(x_i\) is assumed to be Student’s t-distributed and \(X_i\) denotes the market index on the \(i\)-th trading day. The plot below shows the country-specific \(x_i\)’s.

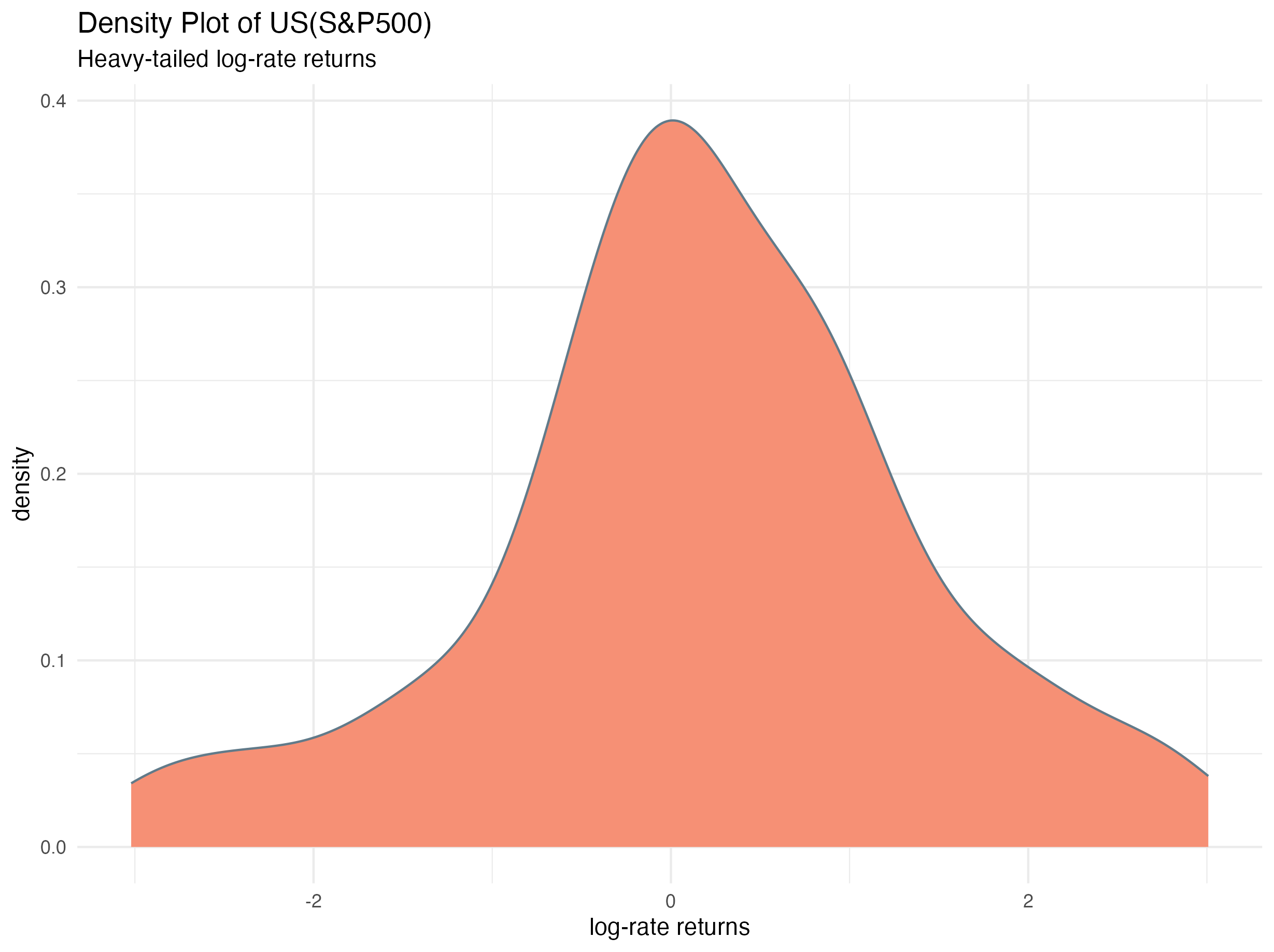

The density plot of the log-rate returns for United States (S&P500) illustrating the heavy-tailed nature of the observations is given below:

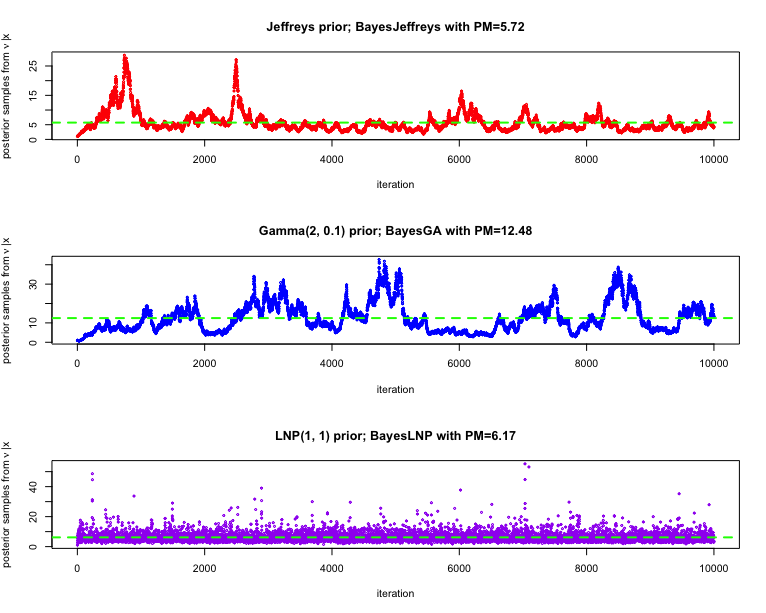

We considering running the (i) MALA sampler for the

Jeffreys prior over \(\nu\), i.e., using

BayesJeffreys for sampling \(S=10000\) posterior samples, (ii)

RWM algorithm for the Gamma prior over

\(\nu\) (with shape and rate

hyper-parameters specified as, \(2\)

and \(0.1\) respectively), i.e., using

BayesGA for sampling \(S=10000\) posterior samples, and (iii)

ESS algorithm for the Log-normal prior

over \(\nu\) (with mean and variance

hyper-parameters specified as \(1\)),

i.e., using BayesLNP for sampling \(S=10000\) posterior samples.

library(dplyr)

# loading the log-rate returns data

data(index_return)

# filtering out the data specific to United States (S&P500)

index_return_US <- filter(index_return, Country == "United States")

x = index_return_US$log_return_rate

# Jeffreys prior over the degrees of freedom

nu_jeffreys = BayesJeffreys(x, S = 10000, sampling.alg = "MALA")

# posterior mean (pm) estimate

nu_jeffreys_pm = mean(nu_jeffreys)

# Gamma prior over the degrees of freedom

nu_gamma = BayesGA(x, S = 10000, a = 2, b = 0.1)

# posterior mean (pm) estimate

nu_gamma_pm = mean(nu_gamma)

# Log-normal prior over the degrees of freedom

nu_LNP = BayesLNP(x, S = 10000)

# posterior mean (pm) estimate

nu_LNP_pm = mean(nu_LNP)The trace plots of the posterior samples are given below, for different choices of priors as employed above. The posterior mean estimate of the degrees of freedom is also highlighted in each of the cases.

[1] Lee, S. Y. (2022). The Use of a Log-Normal Prior for the Student t-Distribution. Axioms, 11(9), 462. https://doi.org/10.3390/axioms11090462.